Executive Summary

This white paper provides a concise analysis of methanol’s production and market evolution and highlights Demeter Energy’s differentiated platform for the development of low carbon biomethanol.

Methanol is a mature, globally traded commodity with a century-long production history and well-established end markets. Advances in catalytic conversion, originating with BASF’s early industrial processes and refined through modern low-pressure systems, have created a robust and bankable production platform. This same chemistry now enables the transition from fossil-based methanol to low-carbon alternatives.

Biomethanol is chemically identical to conventional methanol but benefits from a fundamentally different carbon profile. Produced from biomass-derived synthesis gas, it can achieve materially lower lifecycle emissions while remaining fully compatible with existing infrastructure and downstream applications. As regulatory pressure and customer demand accelerate, biomethanol is gaining traction in sectors where decarbonization options are limited, including marine fuels, heavy industry, fuel blending, and chemical intermediates.

Demeter Energy’s biomethanol plants are designed to capitalize on this convergence of proven chemistry and rising low-carbon demand. The facilities target annual production of 100,000 metric tons of ultra-low carbon biomethanol, alongside the capture of approximately 200,000 metric tons per year of biogenic CO₂. The plants leverage a modular technology platform, a Design-Build EPC execution model, and a forestry-residue feedstock strategy to reduce execution risk and enhance scalability. A projected carbon intensity (CI) score of -50 or better positions the asset to benefit from premium pricing, policy incentives, and long-term offtake interest.

For investors, the opportunity is defined by scarcity and durability: methanol markets are established, demand for low-carbon supply is accelerating, and bankable biomethanol capacity remains limited. Demeter Energy aims to deliver scalable, financeable projects positioned at the intersection of energy policy transitions, industrial demand, and infrastructure-ready fuels.

1. Short History

Before industrial syngas processes emerged, methanol was produced mainly through destructive distillation of wood, which is why it became widely known as “wood alcohol”. That legacy route was eventually displaced by synthetic production pathways that were more scalable, more reliable, and less constrained by biomass availability.

The modern methanol industry began in earnest between 1923 and 1925, when BASF commercialized the first successful syngas-to-methanol process using high pressure and zinc-chromium catalysts. This was the critical breakthrough that shifted methanol production from a niche wood-derived product to a major synthetic commodity. By the end of the 1920s, plants around the world were producing only about 42,000 metric tons per year in total, so the market was still niche and mainly tied to chemicals and solvents rather than fuel.

From the 1930s through the 1950s, methanol expanded steadily as production technology improved, and natural-gas-based synthesis spread. The market was still relatively small compared with today, but it was becoming an established feedstock for formaldehyde, acetic acid, and other basic chemicals.

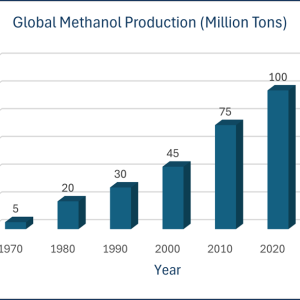

By the 1970s, global methanol production was around 5 million metric tons per year. The 1973 oil crisis also sparked interest in methanol as a transportation fuel, which helped broaden the market beyond traditional chemicals.

By the mid-1990s, worldwide methanol capacity was projected to reach about 30 million tons, showing how much the market had scaled during the petrochemical build-out of the 1980s and 1990s. By 2010, global demand reached 45 million tons.

The biggest growth wave came in the 2010s, especially from China, where methanol use expanded into fuels and methanol-to-olefins. Global demand reached about 75 million tons in 2015, 81 million tons in 2018, and about 98 million tons in 2019.

As of today, the methanol market is roughly 97 million tons according to Methanex, while some 2025–2026 market reports place it around 116–120 million tons depending on whether they are measuring demand, supply, or broader market definitions. In dollar terms, one recent market estimate values the industry at roughly $39–40 billion in 2025–2026. The data in the charts below show the significant increase in methanol production over the last 100 years.

| Period | Approximate Market Size |

| 1920s | Tens of thousands of tons globally |

| 1970s | About 5 million tons |

| 1990s | Around 30 million tons of global capacity |

| 2010 | About 45 million tons of demand |

| Mid- 2010s | About 75 million tons |

| Today | In Excess of 100 million tons, or about a $40 billion market |

Sourced: Methanol Institute

2. Today’s Market

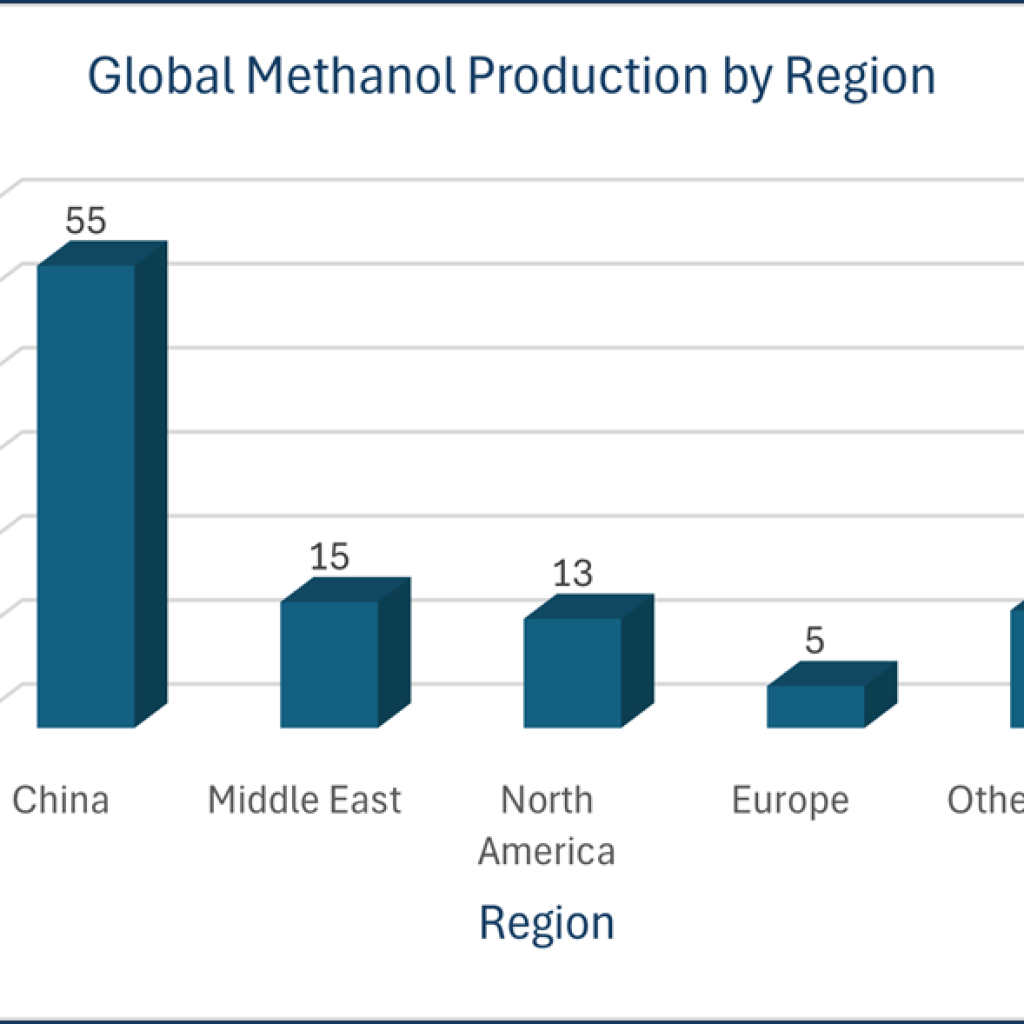

Over ninety major methanol plants operate worldwide, mainly in Asia, especially China, thanks to extensive coal-based capacity. Regions rich in natural gas, like the United States and Middle East, favor gas-based methanol production. The industry is closely tied to petrochemical and fuel markets. The chart below shows the production of methanol by region.

Source: Methanol Institute

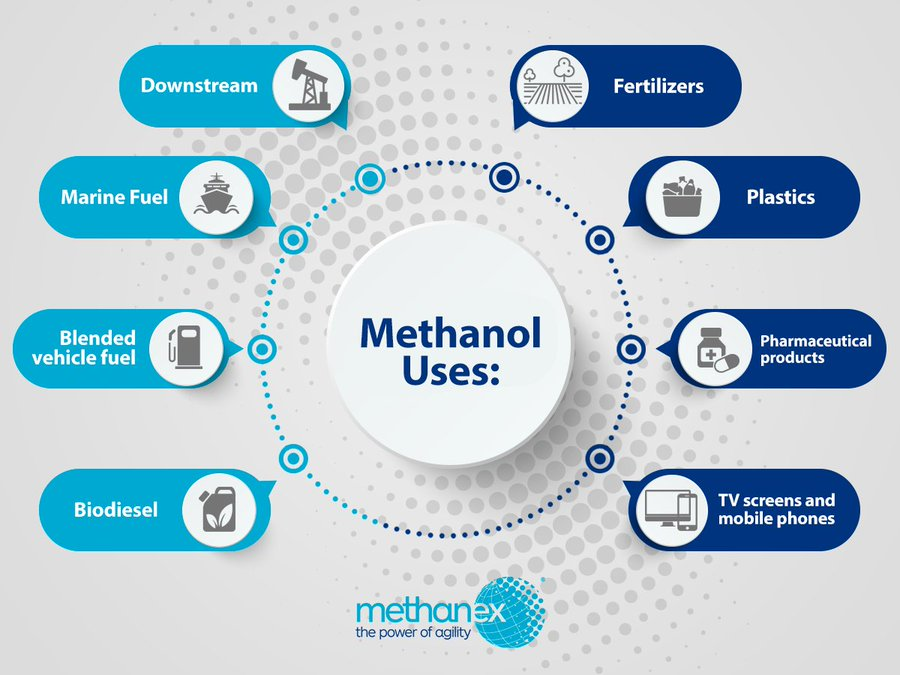

3. Methanol Use by Industry and In Our Lives

Methanol is primarily used as a chemical building block and secondarily as fuel. The table below shows the main end-use industries and approximate shares of global methanol demand. Shares vary slightly by source because some reports group methanol-to-olefins (MTO), direct fuels, and other derivatives differently.

| Industry / Segment | Approx. Share | How Methanol Is Used | Typical End Products / Markets |

| Construction and wood products | ~25% | Converted to formaldehyde resins for adhesives and binders. | Plywood, MDF, particleboard, OSB, laminates, insulation materials |

| Plastics and petrochemicals | ~13-20% | Used in methanol-to-olefins (MTO) to make ethylene and propylene. | Plastic packaging, films, auto parts, appliance housings, synthetic fibers |

| Textiles and polyester / PET | ~10-11% | Used to make acetic acid and downstream intermediates for PTA and acetate chemistry. | Polyester fiber, PET bottles, textile yarns, acetate products |

| Paints, coatings, solvents and inks | ~15-19% | Feeds acetic acid, methylamines, chloromethanes, and solvent chains. | Coatings, inks, resins, solvents, paint removers, specialty chemicals |

| Refining and gasoline blending | ~11-12% | Converted into MTBE and related gasoline blend components. | Higher-octane gasoline and cleaner-burning fuel blends |

| Renewable fuels and biodiesel | ~6% | Used as a reactant in biodiesel production. | Biodiesel for road, industrial, and transport fuel markets |

| Direct fuel, marine, heating and power | ~10% | Used directly as methanol fuel or via dimethyl ether (DME). | Marine fuel, industrial boilers, kilns, cookstoves, backup power |

Sources: Methanex 2024 Annual Report; Methanex Investor Presentation (July 2025), methanol demand applications; IRENA Innovation Outlook: Renewable Methanol.

4. Chemical Industry

Methanol is one of the chemical industry’s core building-block molecules. It is valued as a low-cost, liquid C1 feedstock that can be transported globally and converted into high-volume intermediates. Today, traditional chemical uses still account for roughly half of world methanol demand, and additional volumes are converted through MTO into ethylene and propylene for plastics and fibers.

Chemical industry relies on methanol because it is easy to store and ship, reacts efficiently in large-scale process chemistry, and can be sourced from natural gas, coal, biomass, biogas, or captured CO₂ plus hydrogen. That makes methanol both a major conventional petrochemical feedstock and a potential lower-carbon platform molecule for future chemical production.

5. Methanol as a Fuel: Market Size and Feedstock Breakdown

In the methanol market, two common questions arise: (1) the volume of methanol used for fuel and energy, and (2) the sources: coal, natural gas, or biomass, from which methanol is produced. Below is the breakdown.

| Fuel / energy market (broad definition) | About 29–30 million tonnes per year, based on ~97 Mt global demand in 2024 and energy-related applications of just over 30%. |

| Fuel applications (narrow definition) | About 19 million tonnes in 2024. This narrower measure excludes some fuel intermediates depending on methodology. |

| What’s the difference | The broad measure includes buckets such as MTBE, DME, biodiesel, and direct fuel use; the narrow measure is closer to direct fuel and tightly defined fuel applications. |

Production by feedstock

Current public market data show global methanol production remains overwhelmingly fossil-based. Using the current industry forecast basis of roughly 100 Mt of demand, the supply mix is approximately 59 Mt from natural gas, 40 Mt from coal, and less than 1 Mt from biomass/other green feedstocks.

How fossil-derived syngas became dominant

Natural gas reforming emerged as the leading methanol route in the United States and in much of the world because it produces a comparatively clean, hydrogen-rich syngas that is highly suitable for methanol synthesis. Natural gas also enabled large, efficient plants with strong economies of scale, especially in regions with abundant low-cost gas supplies.

Coal gasification became especially important in coal-abundant regions, most notably China. In these markets, coal-based methanol production provided a way to monetize domestic resources and support large downstream value chains for formaldehyde, acetic acid, olefins, plastics, and other industrial chemicals.

Residual oil, petroleum coke, and other hydrocarbons can also be converted into syngas, but these pathways have typically remained secondary. In most cases, they have been less attractive than natural gas reforming or coal gasification because of feedstock quality, operating complexity, emissions profile, or economics.

Why fossil pathways dominated for decades

Several structural advantages kept fossil pathways in the lead for decades:

- Higher energy density and more predictable feedstock composition, which simplifies plant design and improved operating reliability.

- Steam reforming and gasification technologies matured over many decades, reducing technical risk and benefiting from continuous process optimization.

- Strong demand growth for methanol as a precursor to formaldehyde, acetic acid, MTBE, olefins, and plastics favored feedstock routes capable of supplying large and reliable volumes.

- Fossil-based methanol generally had a lower production cost than biomass-based alternatives, especially before carbon policy; renewable fuel incentives, and green-product premiums began to influence project economics.

Bottom line: fossil-derived syngas became dominant because it matched the needs of a fast-growing methanol industry: large-scale production, stable chemistry, proven process technology, and lower cost. That legacy still shapes the global market today, even as biomethanol and other low-carbon pathways begin to expand.

6. Fossil Methanol and Biomethanol: Same Molecule, Different Carbon Pathway

Fossil methanol and biomethanol are chemically identical and can serve the same end uses. The practical difference lies upstream, in the source of carbon, the complexity of syngas generation, and the resulting carbon intensity profile.

| Dimension | Fossil Methanol | Biomethanol | Implication |

| Primary feedstocks | Natural gas, coal, or oil-derived streams | Biomass such as forestry residues, agricultural residues, waste streams, or energy crops | Feedstock source drives lifecycle emissions and sustainability profile |

| Syngas preparation | Well-established reforming or gasification routes | Gasification with more demanding cleanup and conditioning | Biomass variability adds operational complexity |

| Carbon intensity | High lifecycle carbon intensity from fossil carbon | Potentially near-carbon-neutral or lower when based on sustainable biomass | Lower CI supports premium pricing and compliance value |

| Industry maturity | Massive infrastructure base and large existing scale | Earlier-stage scale-up with fewer projects | Low-carbon supply remains relatively scarce |

Biomethanol uses the same catalytic synthesis loop as conventional methanol, but its syngas come from biomass gasification rather than fossil reforming or fossil-based gasification. That distinction creates both opportunity and complexity. Biomass is more variable, contains higher impurity loads, and generally requires more demanding gas cleanup. At the same time, the carbon in the product can be associated with renewable or waste-derived biological sources rather than fossil sources.

For that reason, biomethanol is not a new molecule. It is a new strategic positioning of a familiar molecule within the energy transition.

7. History and Growth of the Biomethanol Market

Biomethanol has evolved from a small niche fuel and specialty chemical into an early-stage growth market. For years, commercial activity was limited to a handful of European producers. In the mid-2020s, project development accelerated as shipping decarbonization, low-carbon fuel policies, and demand for lower-carbon chemical feedstocks began to create real market pull.

How the market developed

The earliest biomethanol volumes were produced from biomass-derived streams such as black liquor, biogas, and other biogenic residues. Commercial momentum was modest for many years because fossil methanol remained cheaper and was supported by mature global infrastructure.

One of the most visible early pioneers was BioMCN in the Netherlands. Public industry sources note that BioMCN, founded in 2006 and later acquired by OCI, was producing nearly 60,000 tons of renewable methanol in 2017, largely for European transport fuel markets. That period showed that biomethanol was technically and commercially possible but still operating at a very small scale.

At the start of the 2020s, global renewable methanol output remained limited. IRENA and industry sources indicated that total renewable methanol production was still below about 0.2 million tons per year in 2021, with only a handful of operating plants. In other words, biomethanol had proven the concept, but the market had not yet reached broad commercialization. The table below shows the increase in announced renewable methanol projects.

| Period | Indicative Data Point | What It Shows |

| 2017 | ~60,000 tons from BioMCN | Early commercial-scale proof that renewable methanol could be sold into transport fuel markets. |

| 2021 | <0.2 Mt global renewable methanol output | The market remained very small, with only limited operating capacity worldwide. |

| Feb. 2025 | 210 renewable methanol projects; 16.3 Mt announced biomethanol capacity by 2030 | Development activity began to accelerate sharply. |

| Nov. 2025 | 252 renewable methanol projects; 23.3 Mt announced biomethanol capacity by 2030 | Project announcements expanded quickly, although announced capacity is not the same as operating supply. |

8. Policy Drivers and Market Demand for Low-Carbon Methanol

The accelerating development of renewable methanol markets is not occurring in isolation. It is being driven by a combination of regulatory policy, corporate decarbonization commitments, and structural changes within the global shipping industry.

Among these forces, the maritime sector has emerged as one of the most significant catalysts for low-carbon methanol adoption. Shipping accounts for a meaningful share of global greenhouse gas emissions, and governments, regulators, and major cargo owners are increasingly requiring reductions in lifecycle emissions associated with marine transport.

These developments are creating strong incentives for alternative marine fuels capable of reducing emissions while remaining compatible with existing shipping infrastructure.

Global Policy and Corporate Drivers

Several international and regional policy frameworks are shaping the transition toward lower-carbon marine fuels.

The International Maritime Organization (IMO) has established a long-term objective of achieving net-zero greenhouse gas emissions from international shipping by 2050. Achieving this goal will require significant reductions in fossil fuel consumption across the global shipping fleet.

In Europe, the FuelEU Maritime regulation introduces mandatory reductions in the greenhouse gas intensity of energy used on board vessels calling at European ports. These requirements began in 2025 and tighten progressively over time.

In the United States, renewable fuel policies such as the Renewable Fuel Standard (RFS) and federal clean energy incentives support investment and production of low-carbon fuels.

Beyond regulatory mandates, large multinational corporations are also placing pressure on logistics providers to reduce supply-chain emissions. Companies including Microsoft, Google, Amazon, IKEA, Unilever, Michelin, DuPont, and Target have all committed to reducing the carbon footprint of transportation associated with their global operations.

Together, these regulatory frameworks and voluntary corporate commitments are accelerating the transition toward alternative marine fuels.

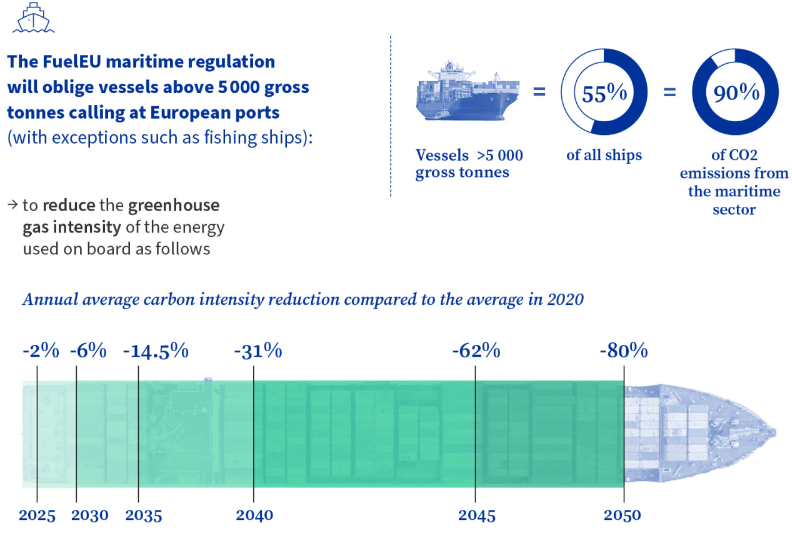

FuelEU Maritime and Shipping Decarbonization Targets

FuelEU Maritime represents one of the most concrete regulatory mechanisms driving the adoption of lower-carbon fuels in shipping.

As the chart below shows, the regulation applies to vessels above 5,000 gross tons calling at European ports, a group that accounts for approximately 55% of the global shipping fleet and roughly 90% of maritime CO₂ emissions. The regulation establishes progressively stricter limits on the greenhouse gas intensity of energy used by ships. These targets begin with a 2% reduction in 2025 and increase steadily to 80% by 2050 relative to a 2020 baseline.

These declining carbon intensity limits effectively require the maritime industry to transition away from conventional fossil fuels toward alternative fuel pathways capable of meeting long-term emissions reduction targets.

Among the available options, methanol has emerged as a leading candidate because it is a liquid fuel that can be stored, transported, and bunkered using infrastructure already established within the global shipping industry.

Growth of Methanol-Capable Shipping Fleet

In parallel with evolving policy frameworks, the global shipping industry has begun investing heavily in vessels capable of operating on alternative fuels.

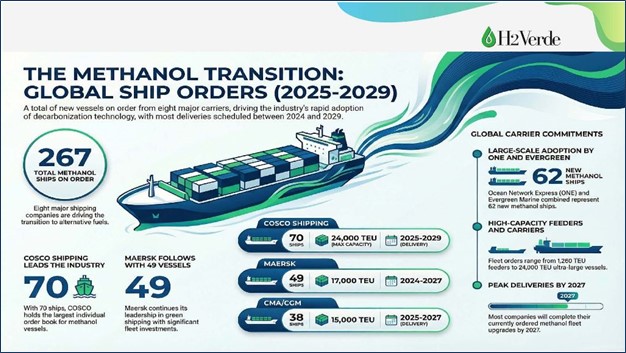

Orders for methanol capable container ships and vehicle carriers capable of operating on methanol have increased rapidly in recent years. Between 2025 and 2029, the number of vessels delivered or on order expanded sharply, reaching more than 267 ships globally, with many more projected to be ordered.

This rapid increase reflects a fundamental shift within the shipping industry as operators begin preparing fleets for future fuel transitions.

Major container shipping companies—including Maersk, Evergreen, COSCO, CMA CGM, HMM, Mitsui OSK, Stena, Hapag-Lloyd, Matson, APL, ONE, and PIL—have announced investments in methanol-capable vessels.

Industry forecasts suggest that the renewable methanol marine fuel market could grow from approximately $4.3 billion in 2025 to more than $30 billion by 2035, representing a compound annual growth rate approaching 22 percent.

The infographic below shows the global methanol ship orders.

* World Shipping Council (2025); Markets and Markets, Green Methanol Ships Market Report.*

Market Implications

Taken together, policy frameworks, corporate decarbonization commitments, and fleet investments are creating a structural shift in the marine fuels market.

The global methanol industry is already large and supported by established infrastructure. However, renewable methanol production remains limited relative to the scale of emerging demand from shipping and other industrial sectors.

As maritime regulations tighten and the number of methanol-capable vessels continues to grow, demand for lower-carbon methanol is expected to expand alongside these structural changes.

Within this evolving market environment, the availability of reliable renewable methanol supply will become increasingly important.

The following section outlines how Demeter Energy’s biomethanol platform fits within this broader market transition.

9. Demeter Energy’s Platform for the Development of Biomethanol

Demeter Energy is developing a series of biomethanol production facilities designed to align established methanol synthesis technology with sustainably sourced forestry biomass feedstocks. Each facility is designed to produce approximately 100,000 metric tons per year of ultra-low carbon biomethanol, while capturing approximately 200,000 metric tons per year of biogenic carbon dioxide.

The development strategy is built around a set of structural advantages intended to support both project bankability and long-term commercial strength. This includes access to a deep forestry feedstock supply base, a targeted ultra-low carbon intensity profile, growing compliance-driven demand for low-carbon fuels, and a modular project architecture designed for replication.

Together, these elements form the foundation of Demeter Energy’s biomethanol platform.

9.1 Strategic Feedstock Advantage

A core element of the project’s strength is its reliance on sustainably sourced forestry residues and wood by-products from the Southeastern United States.

The region represents one of the most productive commercial forestry systems in the world, supported by decades of timber management, established harvesting infrastructure, and a mature network of sawmills and timber operators. Southern Yellow Pine forests in the region grow rapidly and are harvested on short rotation cycles, creating a continuous supply of pulpwood, forestry residues, and mill by-products suitable for energy and biochemical conversion.

This feedstock ecosystem provides several structural advantages for biomethanol production:

- large and stable biomass supply

- established timber logistics and harvesting infrastructure

- relatively predictable feedstock pricing compared with many agricultural residues

- strong sustainability certification frameworks such as SFI, FSC, and SBP

Because the Southeastern United States already supports a large forest products industry, biomass feedstocks are produced at scale and are integrated into existing logistical infrastructure. For a biomethanol facility, this creates a stable and regionally concentrated feedstock basin capable of supporting long-term plant operation.

In practical terms, the strength of the regional forestry sector reduces feedstock risk, which is often one of the primary concerns for biomass-based energy projects.

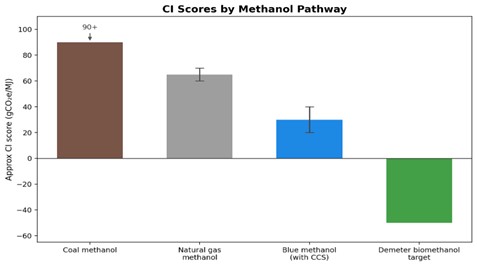

9.2 Carbon Intensity Advantage

The project targets a lifecycle carbon intensity (CI) score of approximately –50 gCO₂e/MJ or lower, depending on the final electricity sourcing strategy and carbon capture configuration.

This performance compares favorably with conventional fossil methanol production pathways. Natural-gas-based methanol typically carries lifecycle carbon intensities in the range of 60–70 gCO₂e/MJ, while coal-derived methanol can exceed 90 gCO₂e/MJ depending on process design and emissions controls.

The resulting carbon intensity differential is significant. Biomethanol produced with sustainably sourced biomass and integrated carbon capture can achieve lifecycle emissions reductions exceeding 100 gCO₂e/MJ relative to many conventional methanol pathways.

This carbon intensity advantage is not simply an environmental metric. It also has commercial implications in markets where fuels and chemical feedstocks are increasingly evaluated on lifecycle greenhouse gas performance. Lower-carbon products qualify for compliance markets, support corporate decarbonization commitments, or command premiums in supply contracts where emissions reductions are valued.

Because biomethanol remains chemically identical to conventional methanol, it can deliver these lifecycle benefits while remaining compatible with existing infrastructure, shipping logistics, and downstream chemical processes.

Sources: California Air Resources Board (CARB); S&P Global Commodity Insights (2025); Methanol Institute (2022); Methanex

9.3 Compliance-Driven Demand Growth

Demand for low-carbon methanol is being driven by structural changes across both fuel and chemical markets.

In maritime transport, regulatory frameworks are increasingly requiring reductions in lifecycle greenhouse gas emissions from marine fuels. Measures such as FuelEU Maritime and the inclusion of shipping within the European Union Emissions Trading System have created incentives for ship operators to transition toward lower-carbon fuel alternatives.

Methanol has emerged as one of the leading candidates in this transition for several reasons. It is a liquid fuel that can be handled using relatively familiar infrastructure, and dual-fuel methanol engines are already being adopted across segments of the global shipping fleet.

Beyond shipping, methanol also plays a critical role in major chemical value chains. Methanol is already embedded in products such as formaldehyde resins, acetic acid derivatives, plastics intermediates, and synthetic fibers, low-carbon methanol offers manufacturers a pathway to reduce lifecycle emissions without fundamentally altering downstream chemistry.

These factors have contributed to growing interest from shipping companies, chemical producers, and fuel suppliers seeking reliable long-term sources of low-carbon methanol.

9.4 Modular Project Architecture and Execution Strategy

Disciplined execution is central to how Demeter Energy develops and delivers new facilities. Our biomethanol facilities are built around a modular process architecture combined with a structured Engineering, Procurement, and Construction (EPC) delivery model.

Through this modular design, key process systems are standardized and fabricated in controlled manufacturing environments before being transported to the project site for installation. This approach reduces on-site construction complexity, improves installation efficiency, and allows facilities to be deployed across multiple locations using consistent equipment configurations. The result is a more predictable development timeline and greater consistency across projects.

Each facility is delivered through a Design-Build EPC structure incorporating fixed-price contracting, defined construction schedules, and performance guarantees. These delivery frameworks are widely used in large-scale energy infrastructure projects and establish clear accountability for construction performance and commissioning outcomes.

For investors and lenders, this approach provides greater transparency around project cost, schedule certainty, and operational ramp-up expectations.

By combining modular engineering with disciplined EPC execution, Demeter Energy establishes a replicable development platform capable of deploying biomethanol facilities at scale, rather than relying on a series of bespoke project builds.

9.5 Carbon Capture and Additional Revenue Pathways

Each Demeter Energy facility is designed to capture approximately 200,000 metric tons per year of high-purity biogenic CO₂ generated during the biomethanol production process.

This carbon stream creates additional commercial optionality beyond methanol sales alone. Potential pathways for the captured CO₂ include:

- permanent geological sequestration

- industrial utilization in chemical or manufacturing markets

- participation in carbon credit frameworks

- qualification for federal incentive structures such as 45Q

Because the captured CO₂ originates from biogenic feedstocks, permanent sequestration can result in net-negative lifecycle emissions for the fuel produced. This can further improve the carbon intensity profile of the biomethanol product and increase its value in markets where lifecycle emissions reductions are monetized.

The integration of carbon capture therefore provides both environmental benefits and potential additional revenue streams, contributing to the overall economic resilience of the project.

Conclusion

Methanol has evolved over the past century into one of the world’s most versatile industrial molecules. Its role as a chemical building block and fuel precursor has created a large and globally integrated market supported by mature production technologies and extensive infrastructure.

The emerging shift toward lower-carbon energy and chemical systems is now creating new demand for methanol produced from non-fossil carbon sources. Biomethanol preserves the established chemistry and logistics advantages of conventional methanol while offering the potential for substantially lower lifecycle emissions.

Demeter Energy’s biomethanol platform is designed to operate at this intersection of established industrial chemistry and emerging low-carbon demand. By combining sustainably sourced forestry feedstocks, ultra-low carbon intensity targets, modular plant design, and integrated carbon capture, the project seeks to deliver scalable biomethanol supply into markets where demand for lower-carbon fuels and chemical feedstocks is increasing.

While biomethanol remains an early-stage segment within the broader methanol market, the convergence of policy drivers, corporate decarbonization commitments, and growing interest in low-carbon fuels suggests that demand for such products may expand significantly over the coming decade.

In this context, projects capable of combining credible feedstock supply, strong carbon intensity performance, disciplined project execution, and flexible commercialization pathways may be well positioned to participate in the next phase of the methanol industry’s evolution.